Insights

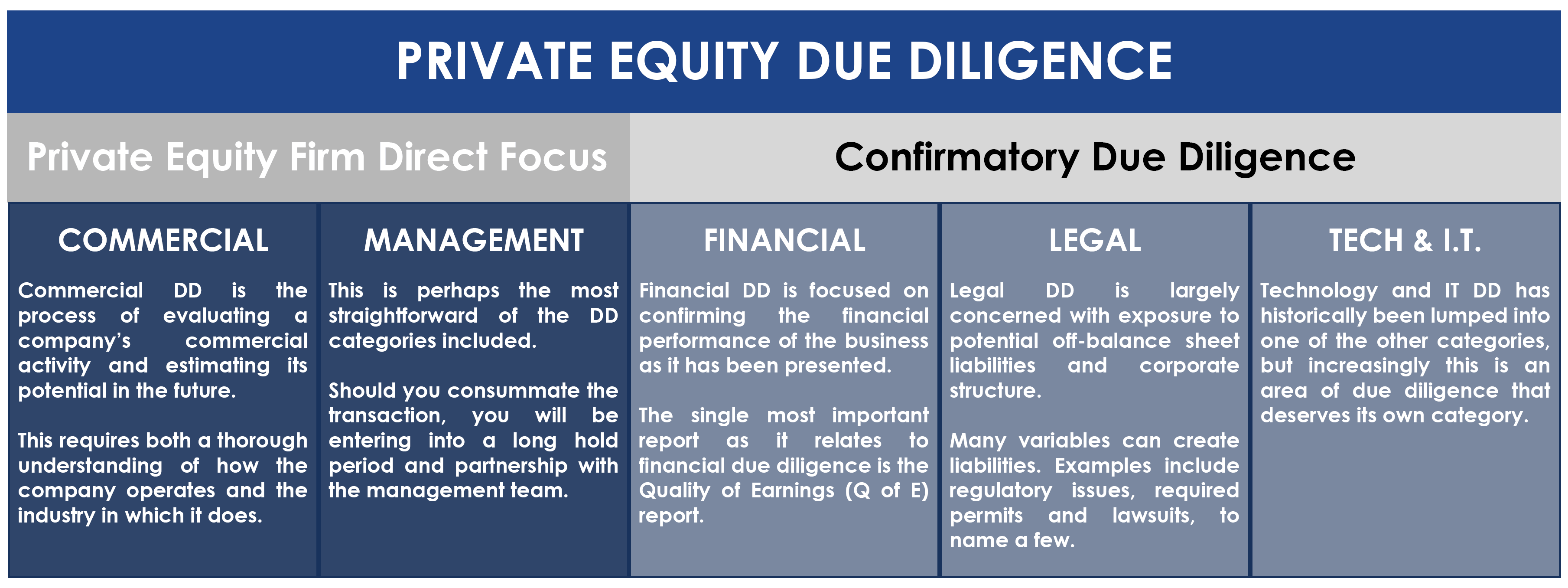

Private Equity: Types of Due Diligence

Private equity due diligence has been traditionally taught with a focus on commercial, financial and legal due diligence. But you will not find a single investor that will downplay the role of management in an operating business, and while information technology (IT) may have been viewed largely as a support function historically, it is increasingly viewed as a driver of growth and value within an organization. For these reasons in this post we will address management due diligence and IT due diligence as well.

Private Equity Deal Sourcing Process

Finding an attractive deal in private equity requires a tremendous amount of work. This video highlights the number of opportunities a private equity firm evaluates before closing a single transaction.

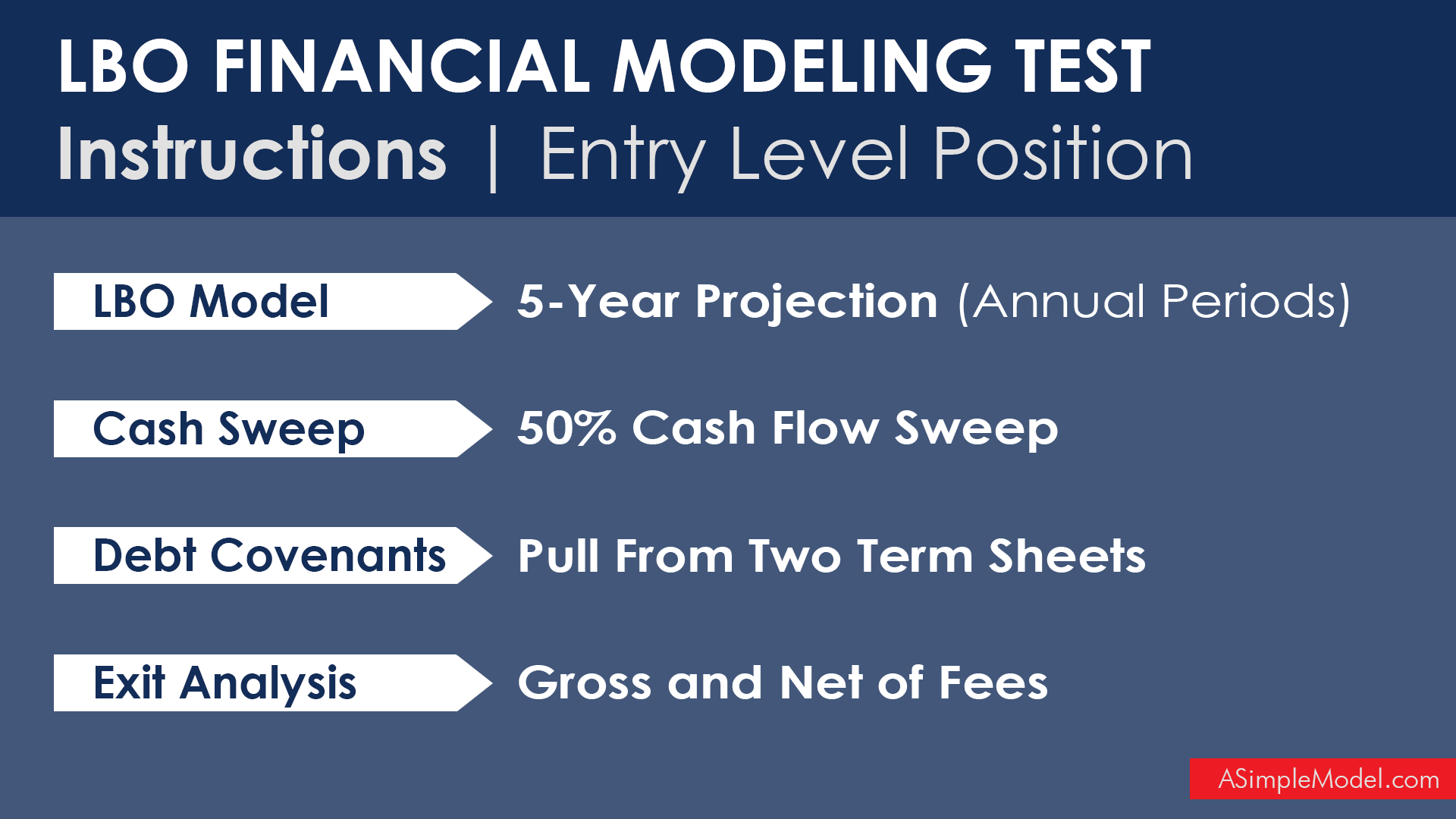

LBO Financial Modeling Test Instructions | Entry Level Position

Securing a job in private equity requires an understanding of LBO models. This case study has instructions for entry-level positions and more advanced positions, but in this post we will focus on the instructions for an entry-level hire.

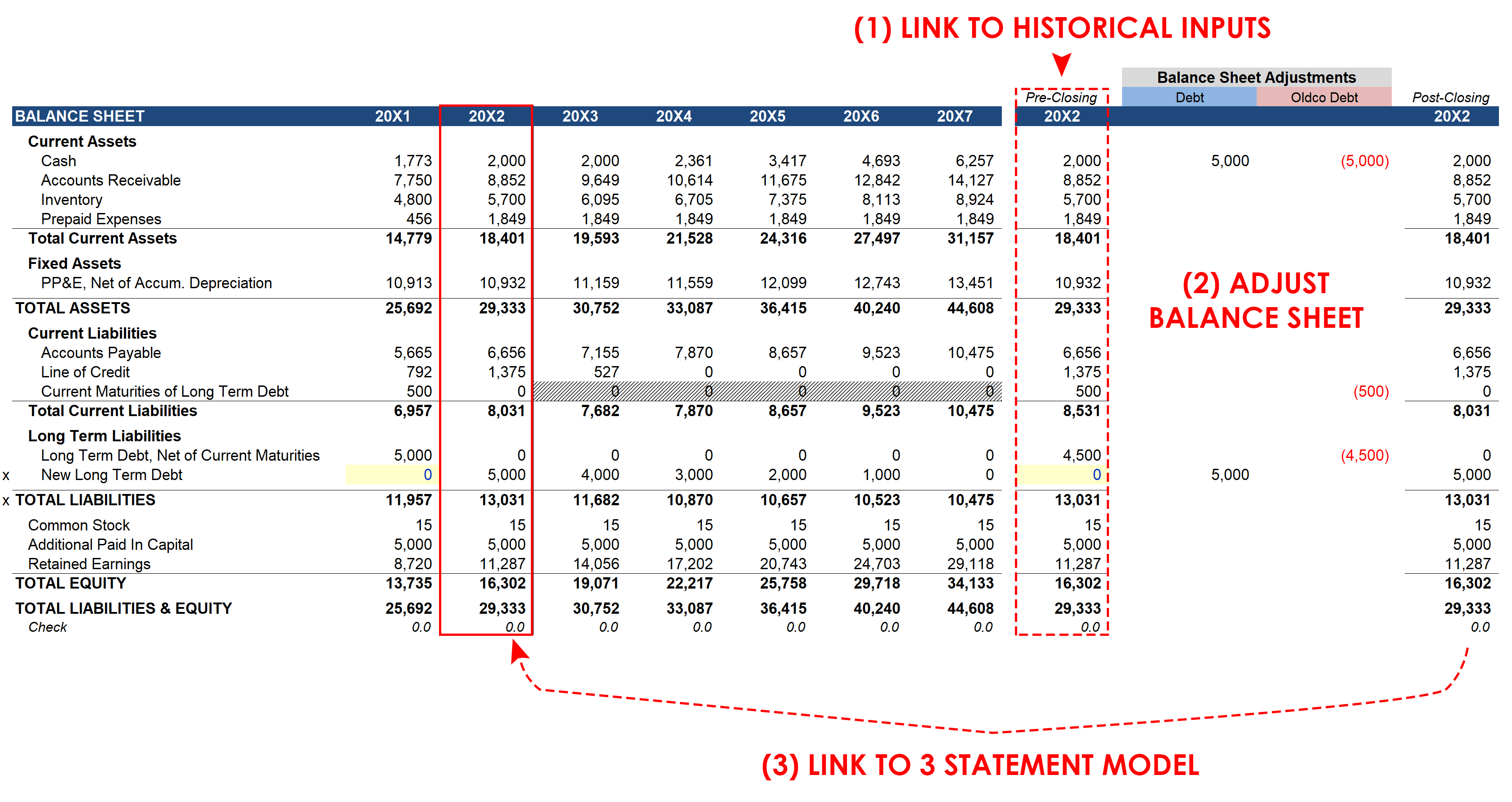

Debt Recapitalization in a Three-Statement Model

In this post we will cover a simple debt recapitalization in a three-statement model. This is a continuation of the post titled “Adding a Loan to a Three Statement Model,” and relies on the same workbook.

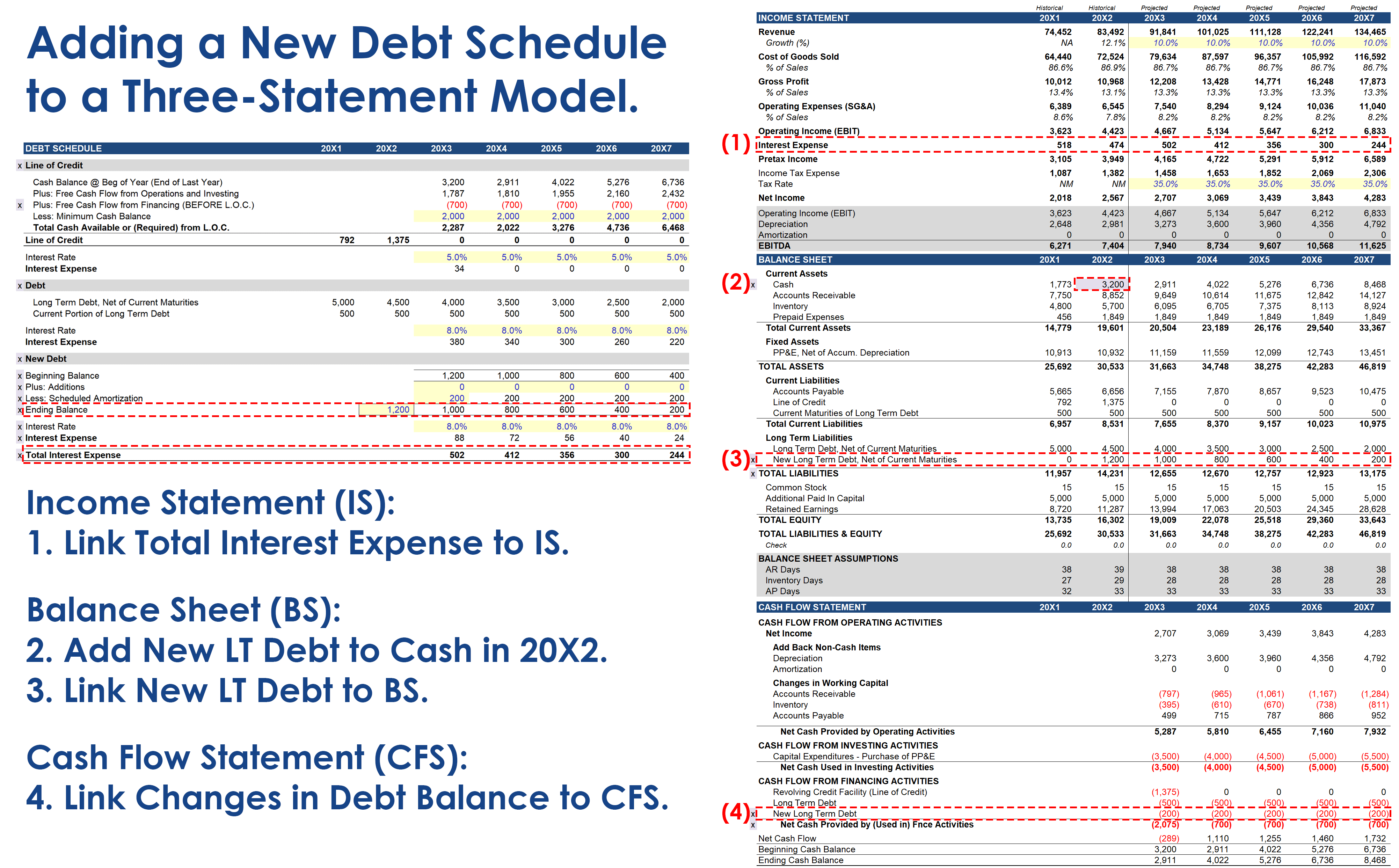

Adding a Loan to a Three Statement Model

In this post we will cover the process of adding a new debt schedule to a three-statement model. For this exercise we will be using the three-statement model built at the beginning of the Integrating Financial Statements video series (template available for download at the bottom of this post).