Insights

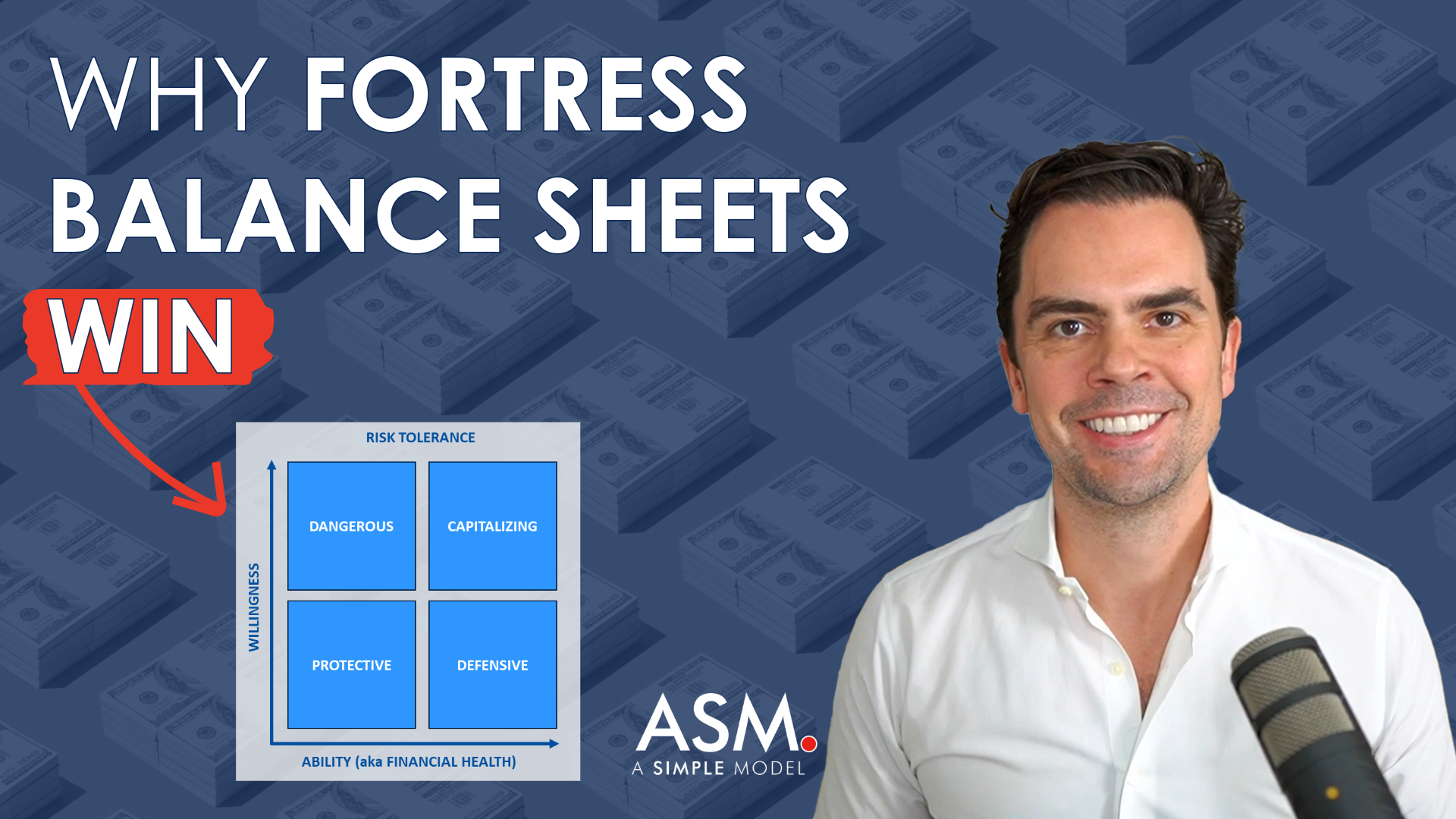

The Power of a Fortress Balance Sheet, Explained Simply

Why a fortress balance sheet matters, and how to explain it without using financial vocabulary to work towards an aligned organization.

AI & Financial Models (Current Thoughts)

AI is coming for financial modelers. The mechanics are automated. Interpretation is not. A look at why fundamentals and judgment are the new edge.

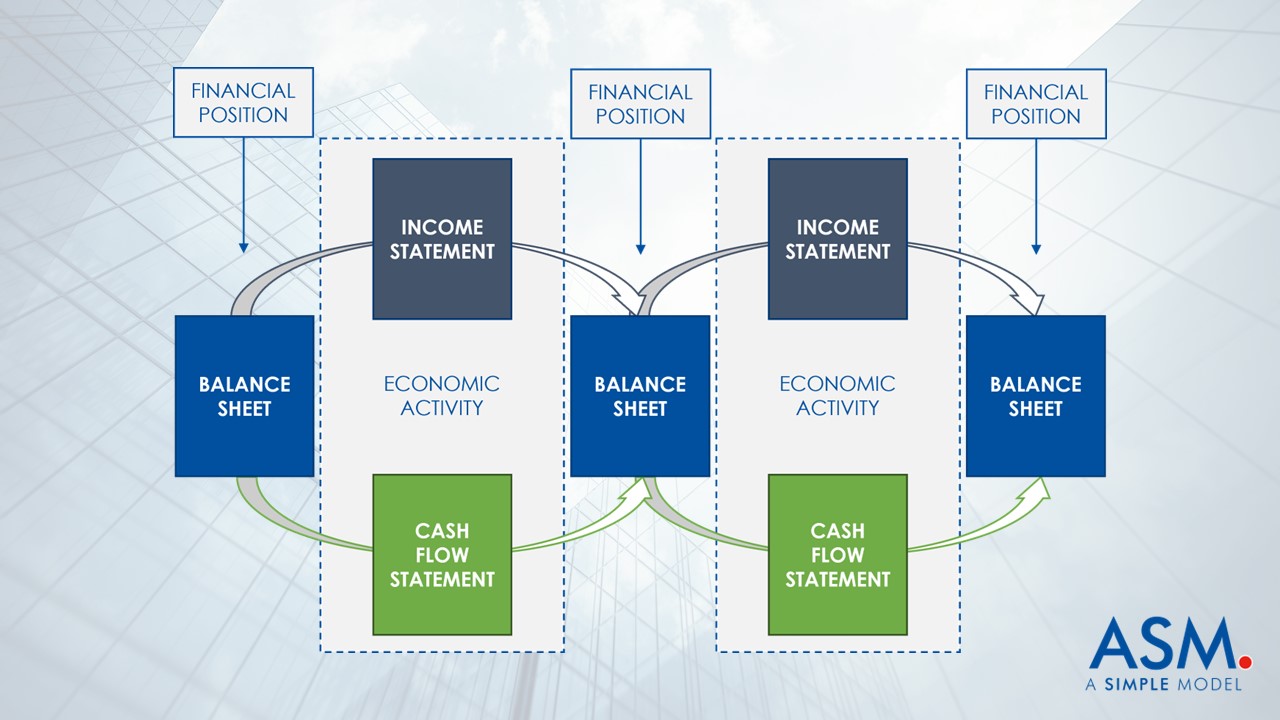

Financial Models: Operating vs Transactional

Learn the difference between an operating financial model and a transactional financial model, and why the three-statement model is critical to both.

Curiosity Builds Speed

How to feel confident in the decisions you make as a business leader: Pair foundational knowledge with speed and flexibility. That’s how you iterate towards success.

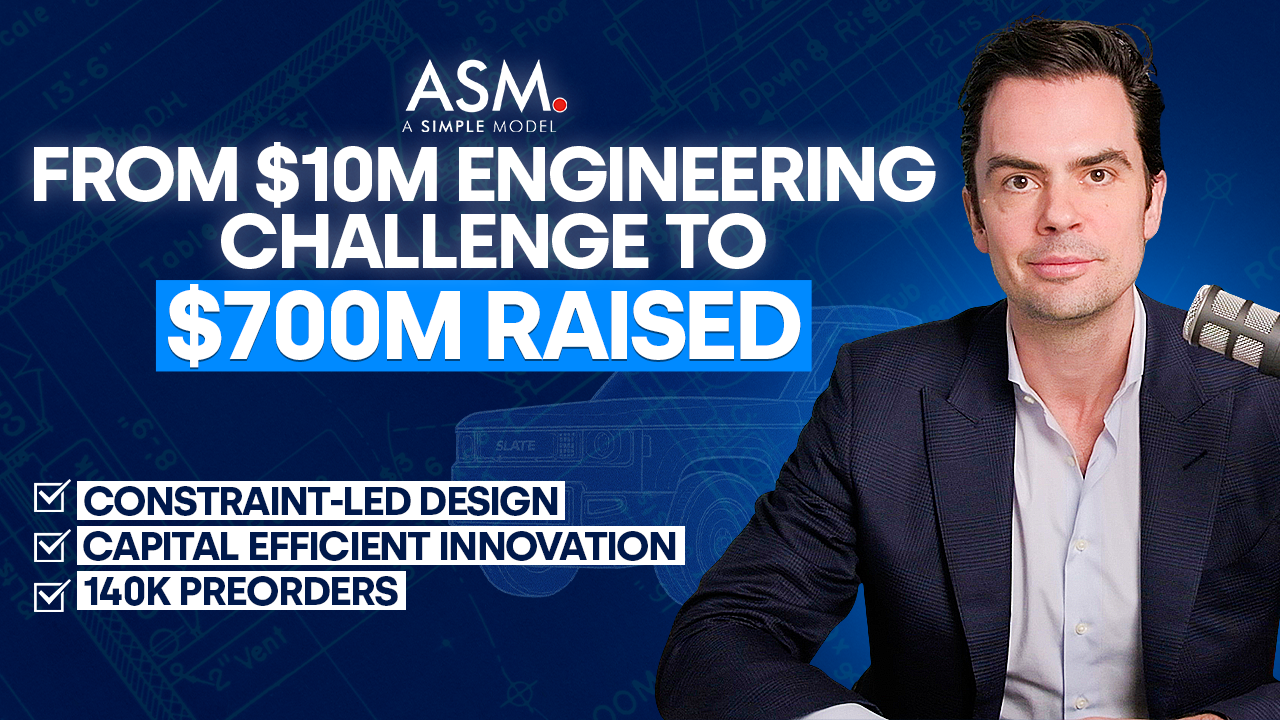

Slate Auto: $10M Challenge to $700M Raise

Most startups bet everything on a single idea. But what if you could build something disruptive before spinning it out? That’s exactly what Re:Build Manufacturing did with Slate Auto: the creators of the $25K electric truck.