The three financial statements are the income statement, the balance sheet, and the cash flow statement. In the video series available on ASM, the financial statements are introduced in the context of building a three-statement model, which provides the foundation for most in-depth financial analysis and valuation work. The objective is not simply to explain what they are, but to demonstrate how they link to each other.

I studied some accounting in college, but there was a problem. Accounting was introduced as the language of business, but the approach made it difficult to see the forest for the trees. It wasn’t until I built my first three-statement model as an investment banker that I felt I truly grasped the big picture. It was a lightbulb moment, which is why I choose to teach it this way on ASM.

Over the years I have heard similar stories from many of the thousands of students that have worked through our content at ASM. And as the testimonial below shows, it may feel like a lot of information initially. But I promise it will come together by the conclusion of this series.

Testimonial: “Having had several accounting courses, initially it seemed odd viewing an entire model in one Excel spreadsheet. It seemed like too much information in one place or on one page and it made me a little uncomfortable, but by the end of the 2nd section I found this to be the most efficient manner that I’ve ever been taught Accounting.”

I would encourage you to review this series even if you have had previous exposure to the three primary financial statements. The lessons are broken down into the chapters that follow.

The Accounting Equation (LINK)

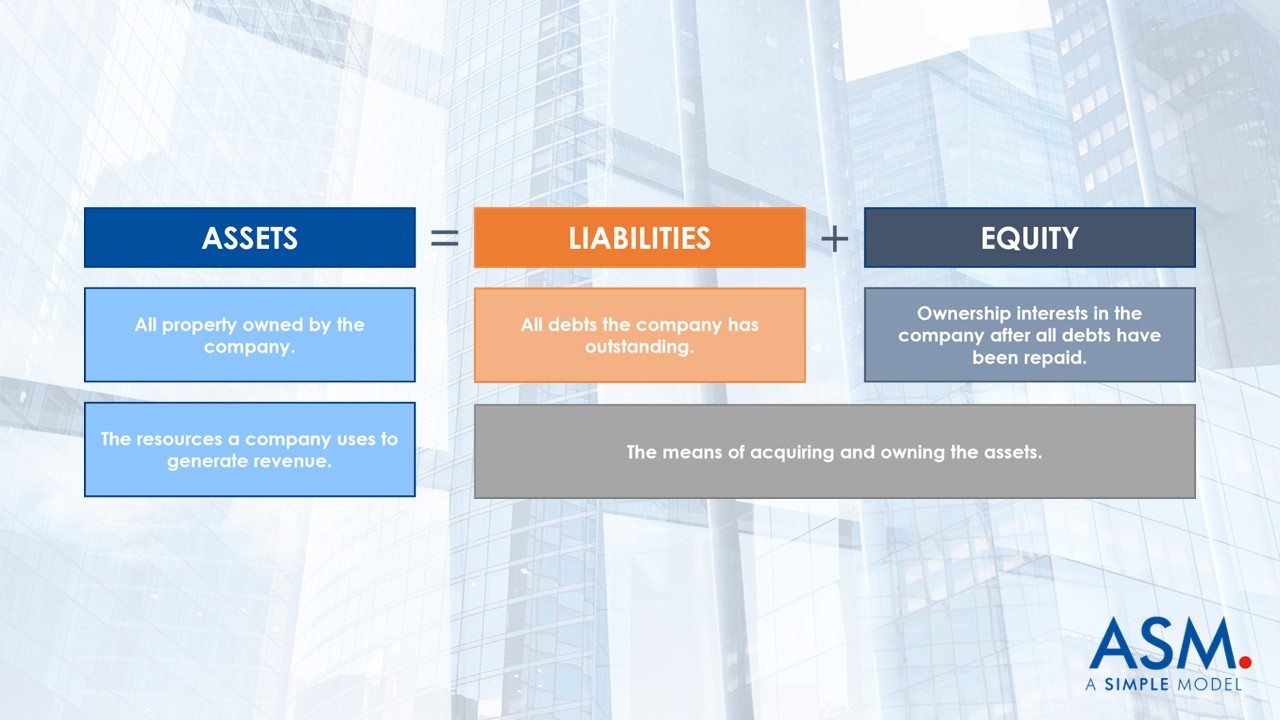

The accounting equation is the first concept you need to master. It’s the foundation on which you can build an array of valuable knowledge and skills. Put simply, the accounting equation states that the value of a company’s assets is equal to the sum of the company’s liabilities and equity.

More precisely, a company uses its assets to generate its revenue; together these represent everything that the company owns. Liabilities and equity represent the means of acquiring and owning those assets. So, on the left-hand side of the equation (assets) you have everything the company owns and on the right-hand side of the equation you have everything the company owes, either to creditors or owners.

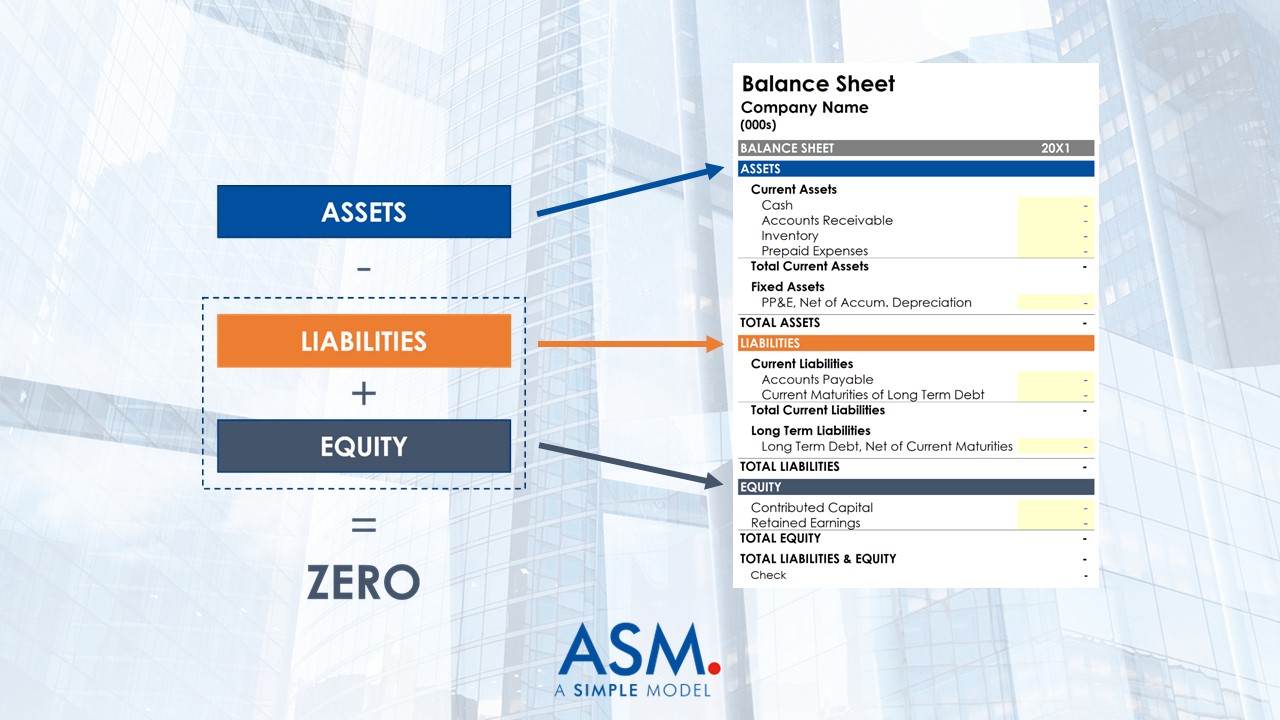

This video explains how the accounting equation is relevant in building financial models. It also provides a cursory overview of double-entry bookkeeping, which is the system most commonly employed by businesses to record financial information. The video concludes by pointing out that the balance sheet is simply a more formal presentation of the accounting equation.

The Balance Sheet (Subscriber Content)

A company’s balance sheet shows its financial position at a given moment in time. Think of it as a “photograph” of the business. You get to see the value of everything the company owns (its assets) and owes (its liabilities and equity).

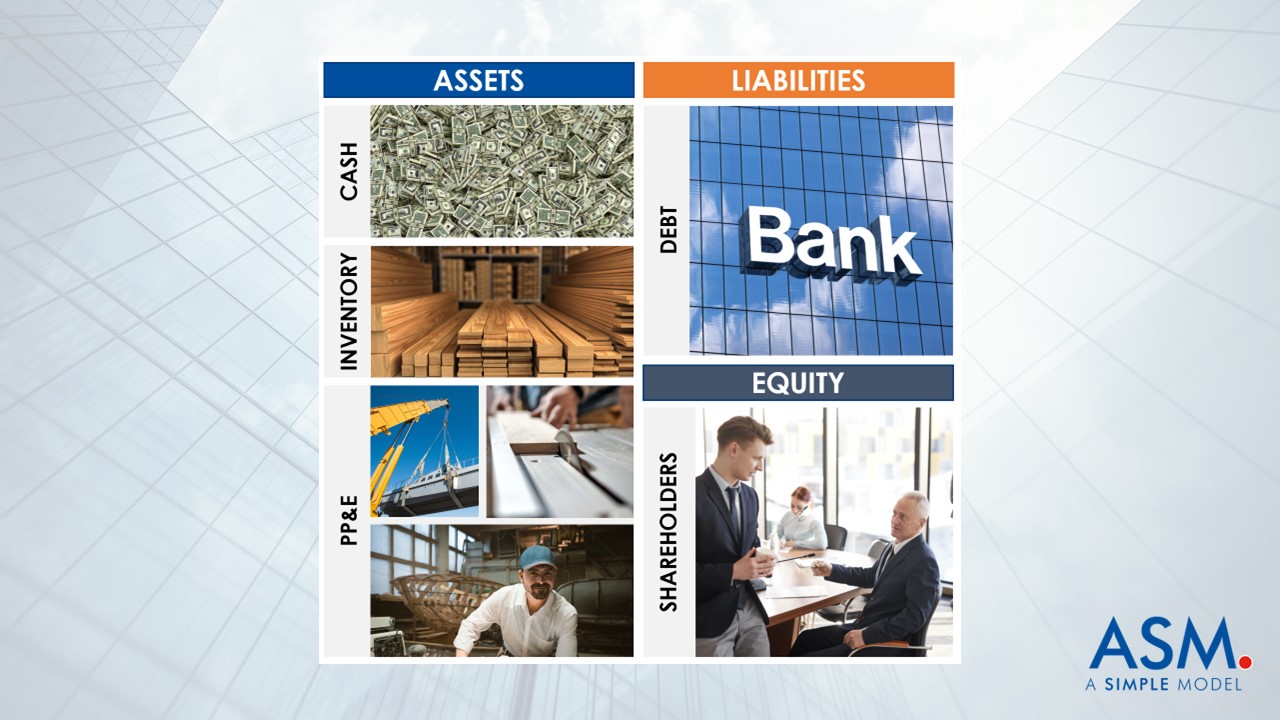

This lesson introduces the balance sheet by asking you to imagine the resources you would require to start a business (see image below), and then to visualize the means of securing these resources (raising debt and equity). By reorganizing these resources, you can see how all of them fall into one of three categories: Assets, Liabilities and Stockholders’ Equity.

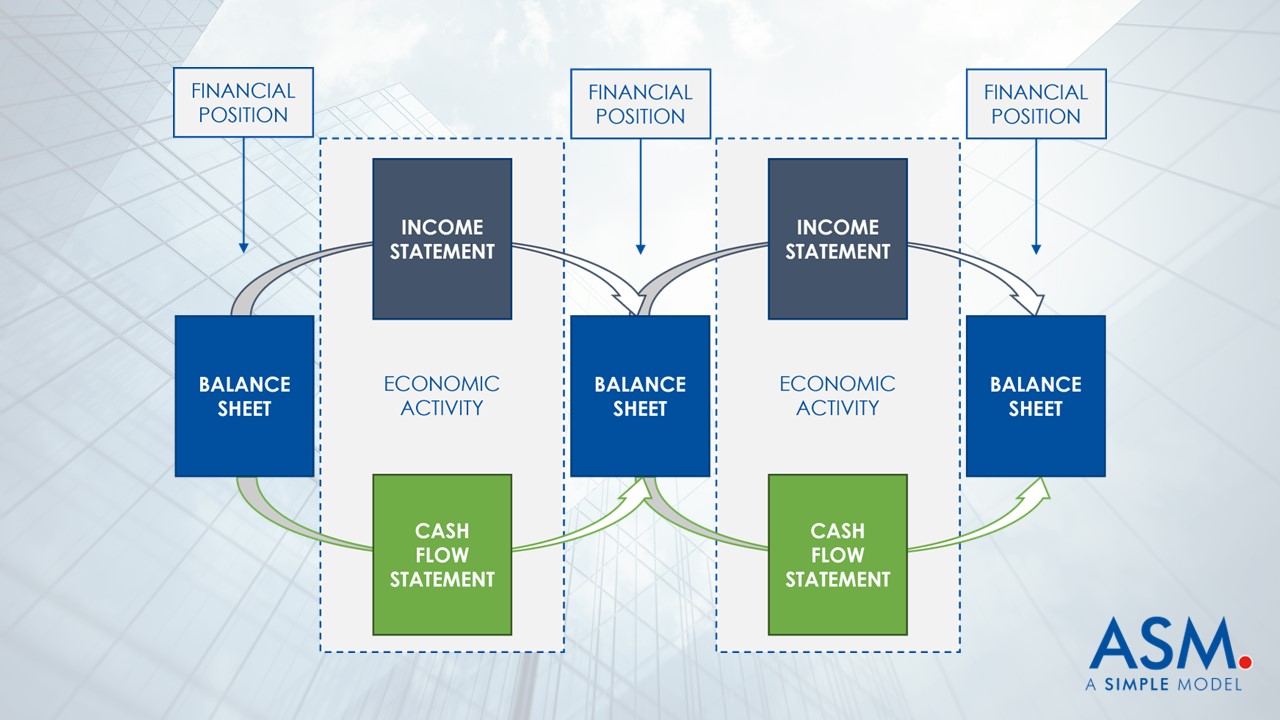

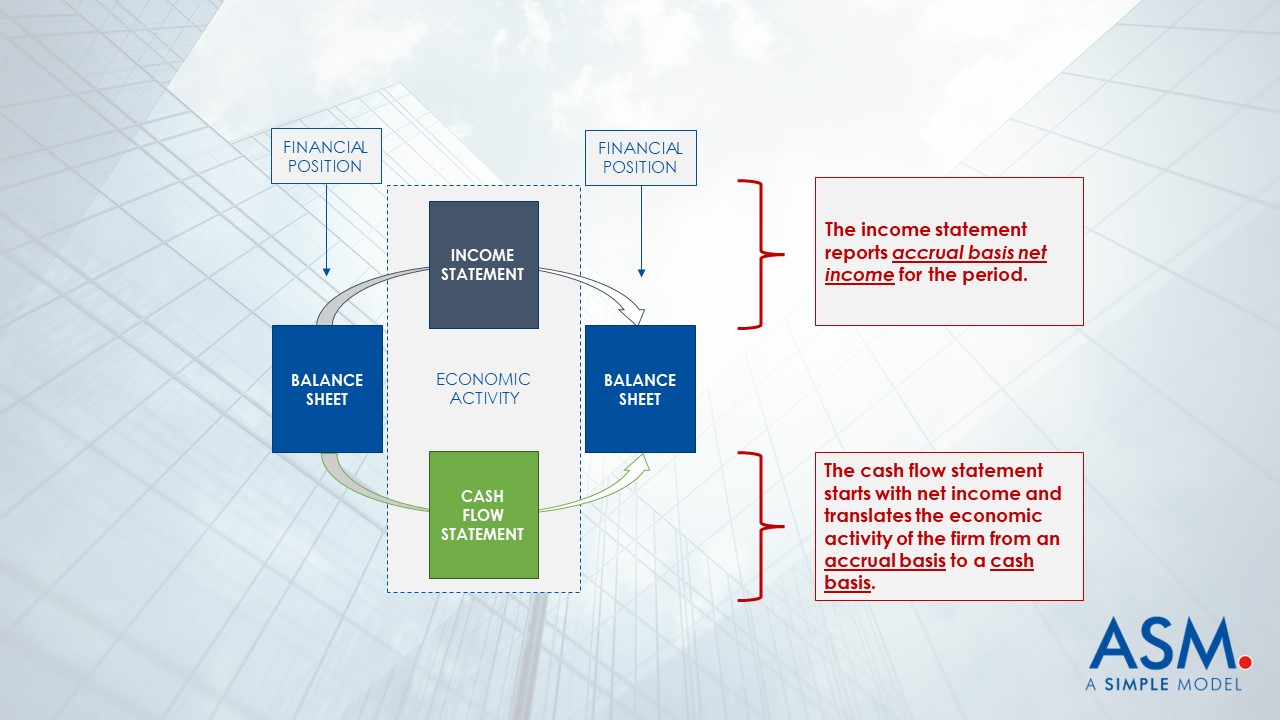

The video then emphasizes that the balance sheet details a company’s financial position at any given time, whereas the income statement and cash flow statement detail the economic activity that has elapsed between periods.

The instruction concludes by highlighting relationships between the balance sheet and other financial statements that are important to keep in mind as you build financial models.

The Income Statement (Subscriber Content)

The income statement shows a company’s revenues (payments the company receives for goods and services) less its expenses (the cost of providing those goods and services). The result, literally the bottom line, is net income.

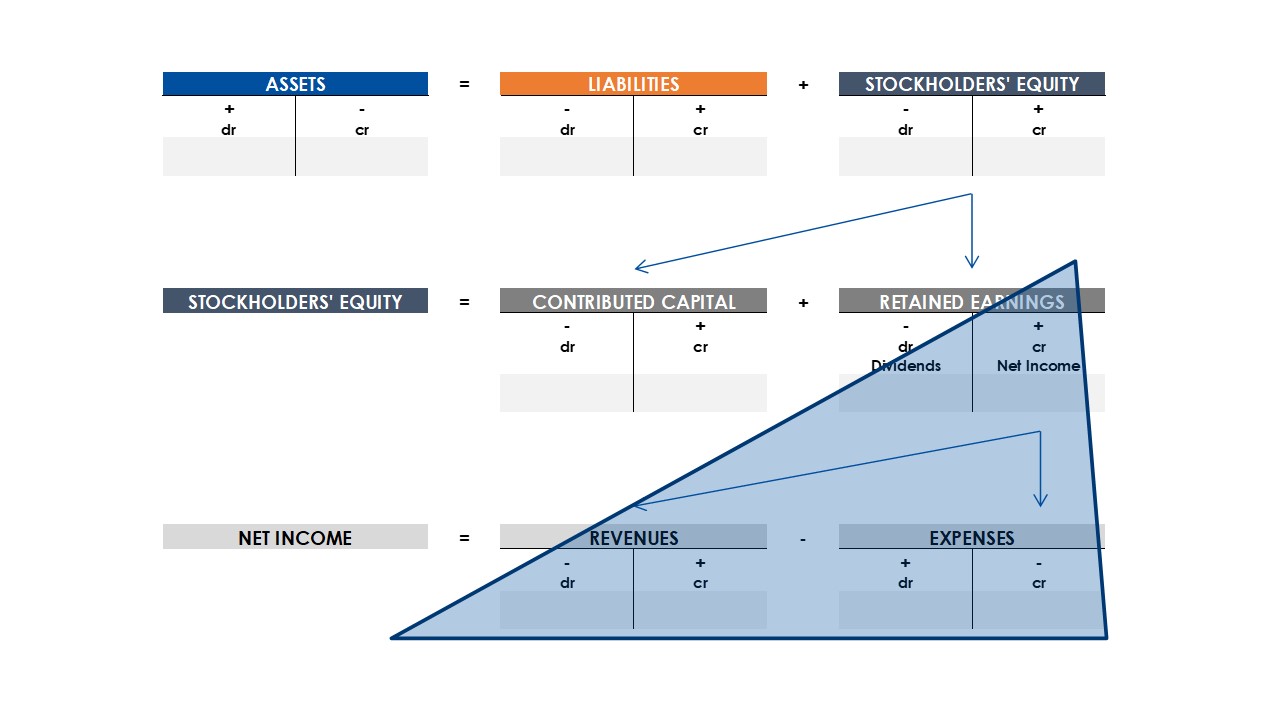

This lesson introduces the income statement by starting with the most concise presentation and expanding on the number of line items. After this introduction the accounting equation is revisited to help illustrate how the balance sheet and income statement relate to one another (blue triangle in the image that follows – the most significant relationship highlighted is that stockholders’ equity grows with net income).

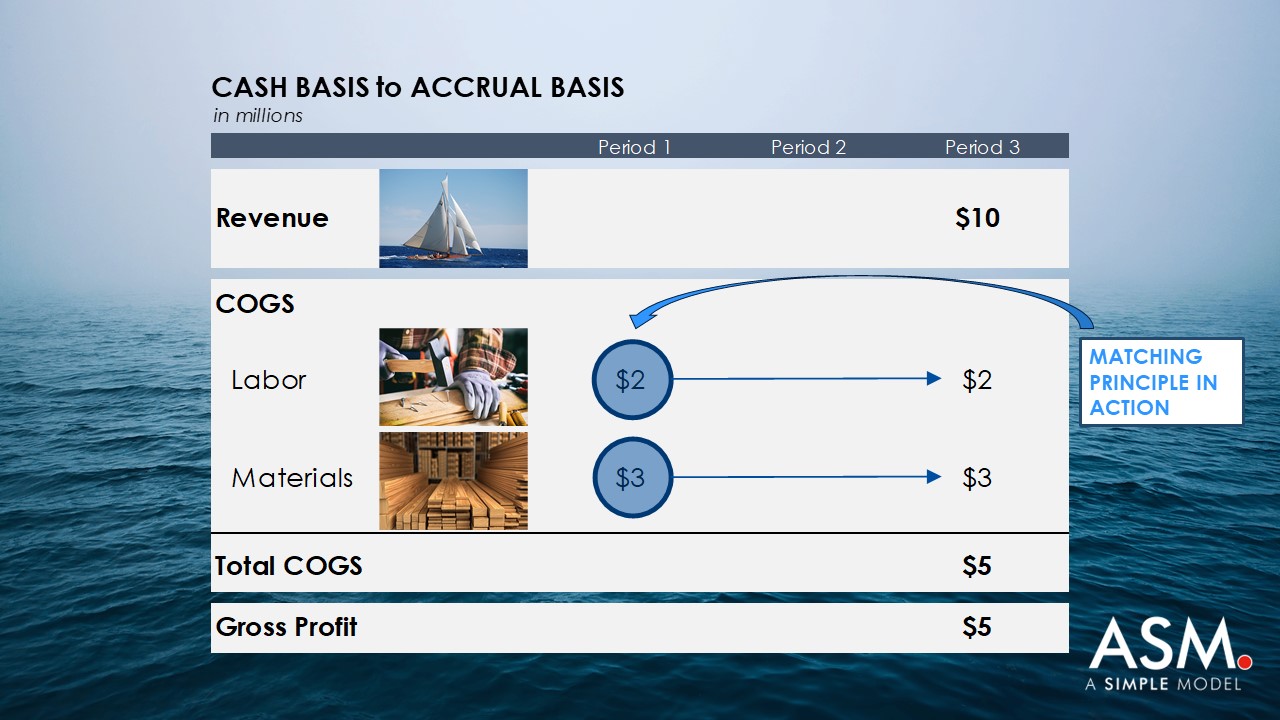

Next the purpose of the income statement is defined, and two important accounting concepts are introduced: the Matching Principle and Depreciation.

The video concludes by highlighting the relationship between the income statement and the cash flow statement and highlighting the difference between an accrual basis of accounting and a cash basis of accounting.

Cash Flow Statement (Subscriber Content)

These lessons introduce the cash flow statement, which is possibly the most straightforward of the three primary financial statements. To focus on how company’s generate cash, the cash flow statement is covered in multiple lessons that tie back to concepts introduced in previously.

Whereas both the income statement and balance sheet reflect an accrual basis of accounting, the cash flow statement starts with net income and translates the economic activity of the firm from an accrual basis to a cash basis.

To demonstrate the difference, the video walks through the purchase of a large piece of equipment on both an accrual and cash basis providing visuals to help cement these concepts.

The video also goes into detail on the three different types of cash inflows and outflows: Cash Flow from Operating Activities, Cash Flow from Investing Activities and Cash Flow from Financing Activities. Using these three categories, the video emphasizes the significance of measuring cash and explains why GAAP measures of profitability in isolation are not sufficient to determine a business’s financial condition.

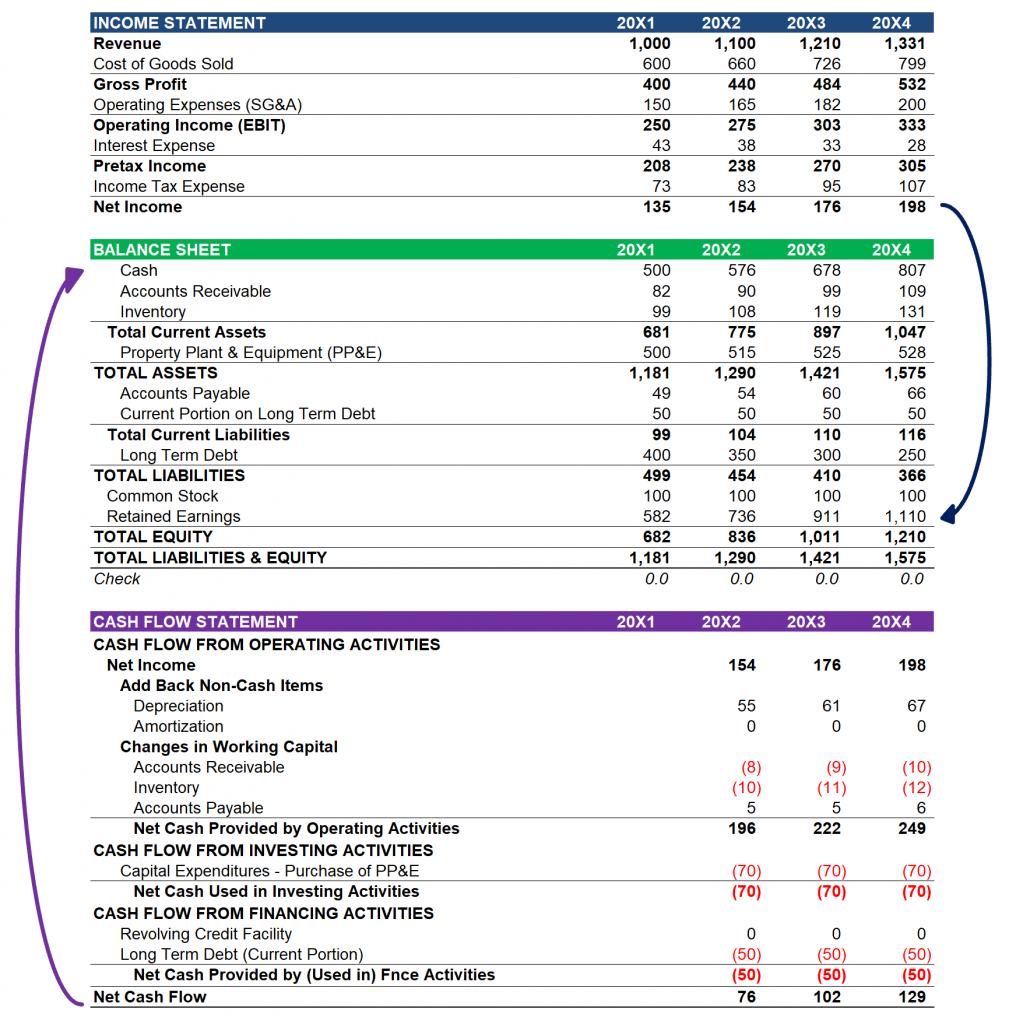

With the introduction of all three financial statements complete, the video then explains how the three financial statements work together to maintain the accounting equation. The first relationship highlighted is that the cash balance calculated on the cash flow statement links to cash on the balance sheet (see arrow on left-hand side of the image below). In this way the cash flow statement adjusts the asset side of your balance sheet in each consecutive accounting period. As a reminder, the video then shows that net income adjusts the equity account (retained earnings) in each accounting period (see arrow on right-hand side of the image below).

With that in mind, recall that the balance sheet is just a formal presentation of the accounting equation. If the cash flow statement adjusts the left-hand side of the equation, or assets, by the company’s cash flow in that period, and the income statement adjusts the right-hand side of the equation, or stockholders’ equity, by net income, then the cash flow statement, which starts with net income, is making adjustments so that the accounting equation holds true. And that is how the accounting equation is balanced in financial models, and therefore how the balance sheet is balanced in financial models.

Learn more about the financial statements and financial statement analysis with the Introduction to Financial Statements course available at ASM.