The leveraged buyout model (LBO) is often viewed as extraordinarily complex, but it shouldn’t be. This video series will teach you how to build an LBO model, and introduce you to purchase accounting, making balance sheet adjustments and detailed debt schedules. It will also really help develop an understanding of capital structure, more so than any other model.

The video series starts by introducing a simple LBO model and then explains how to incorporate more detail. The intention is to create instruction that reinforces all of the relationships that maintain the model as it grows in complexity.

It has been my experience that those new to financial models generally find the LBO model intimidating. In my opinion, this is because most students or analysts are first exposed to more complex LBO models. This is generally done one of two ways:

- In a LBO tutorial that introduces a complex model for a publicly traded company.

- Or worse, presenting someone new to LBO models with a thorough LBO template that needs to be populated.

The first approach introduces too many concepts simultaneously, and the second approach reduces financial modeling to data entry. In contrast, one of the objectives of this video series is to demonstrate that an LBO model is not complicated.

Don’t get me wrong, you can build highly complex LBO models. But this series will demonstrate that a LBO model is just a three statement model adjusted to reflect a transaction. To reflect the transaction you must add three components:

- Source and Uses

- Balance Sheet Adjustments

- Exit Analysis

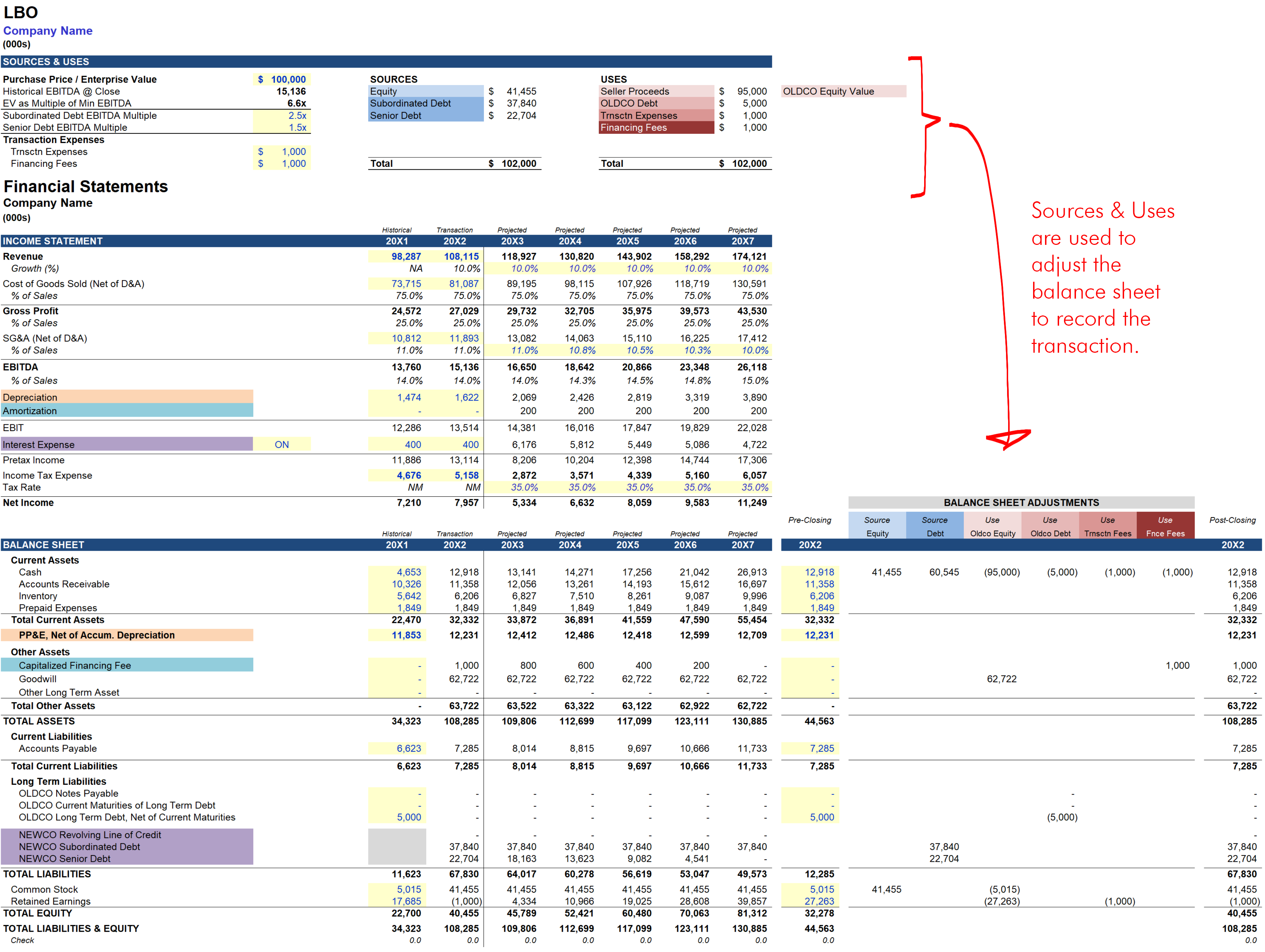

Numbers one and two above will have an impact on your three statement model because these two components are used to record the transaction taking place in your model. How does this work? First, Sources and Uses are used to calculate your Balance Sheet Adjustments (click on the image below for a larger view):

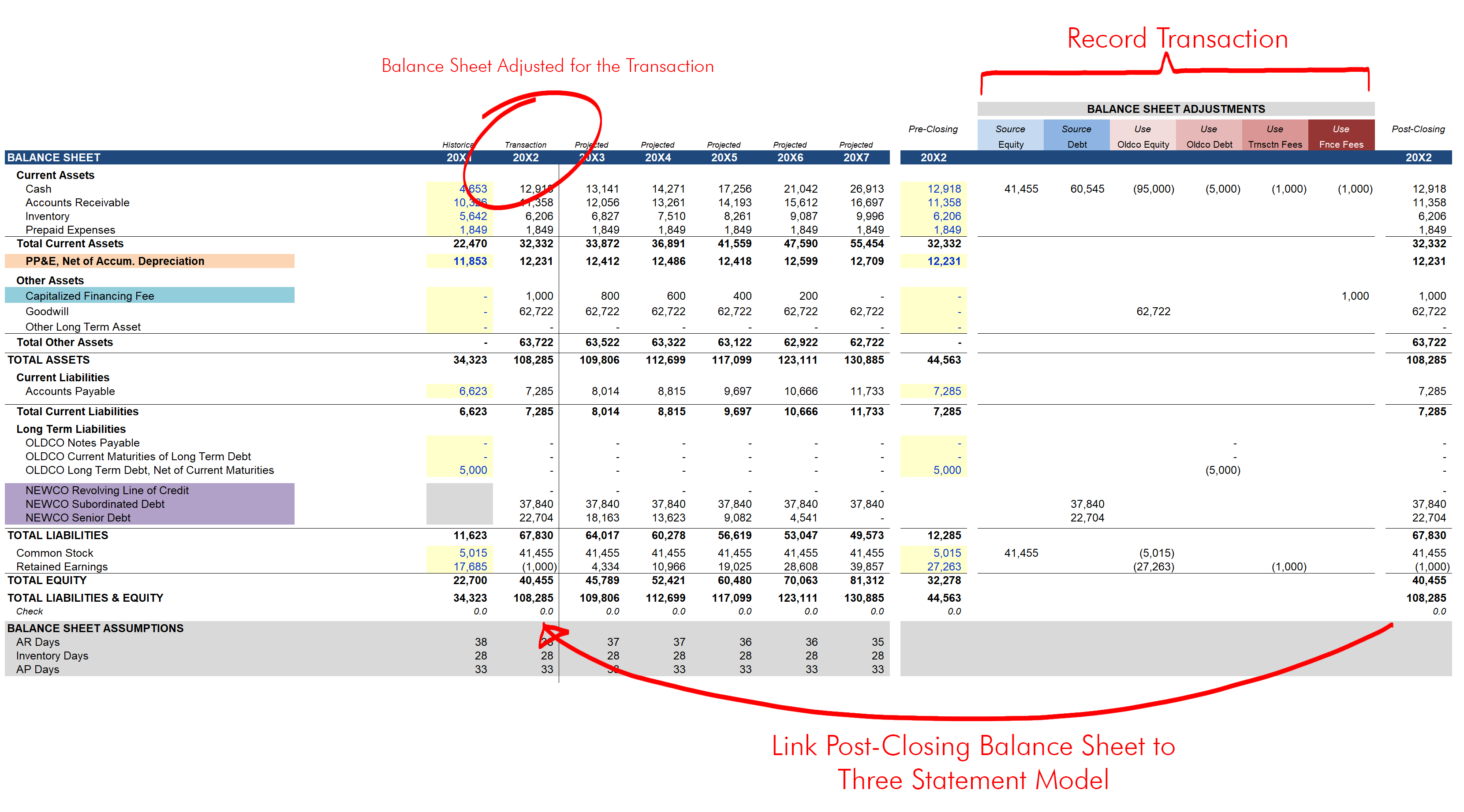

Once the transaction has been recorded under Balance Sheet Adjustments, the “Post Closing” balance sheet is linked directly back to your three statement model (click on the image below for a larger view).

This may sound crazy, but that is the additional layer of complexity. Otherwise building an LBO model is nearly identical to building a three statement model. The only remaining difference is a few new balance sheet line items including the “Capitalized Financing Fee” and “NEWCO” debt items (see video).

I realize we have not touched on the third component yet (“Exit Analysis”), but that is because this section is used to measure the performance of your investment. When you build this part of the model everything under “Exit Analysis” is pulling from the financial statements above. In other words, if you were to highlight and delete every cell under “Exit Analysis” it would not impact the model above. The same cannot be said for “Sources and Uses” or “Balance Sheet Adjustments.” The videos and notes associated with this series will explain everything you need to know about building a proper exit analysis.

Once you have completed the instruction covering how to build a simple LBO model, the video series expands with more detail to introduce the subjects that follow:

Simple LBO: Scenarios & Data Tables (LINK)

This video demonstrates the process of running multiple scenarios through your model, and using data tables to view a range of possible outcomes simultaneously.

Simple LBO: Cash Sweep (1 of 2) (LINK)

This is the first of two videos explaining the cash sweep in a simple LBO model. It requires six quick steps so I chose to capture the process in its entirety. The benefit of an unedited tutorial is that it exposes the small habits and tricks that are otherwise not shared. I hope it makes the material more approachable.

Simple LBO: Cash Sweep (2 of 2)

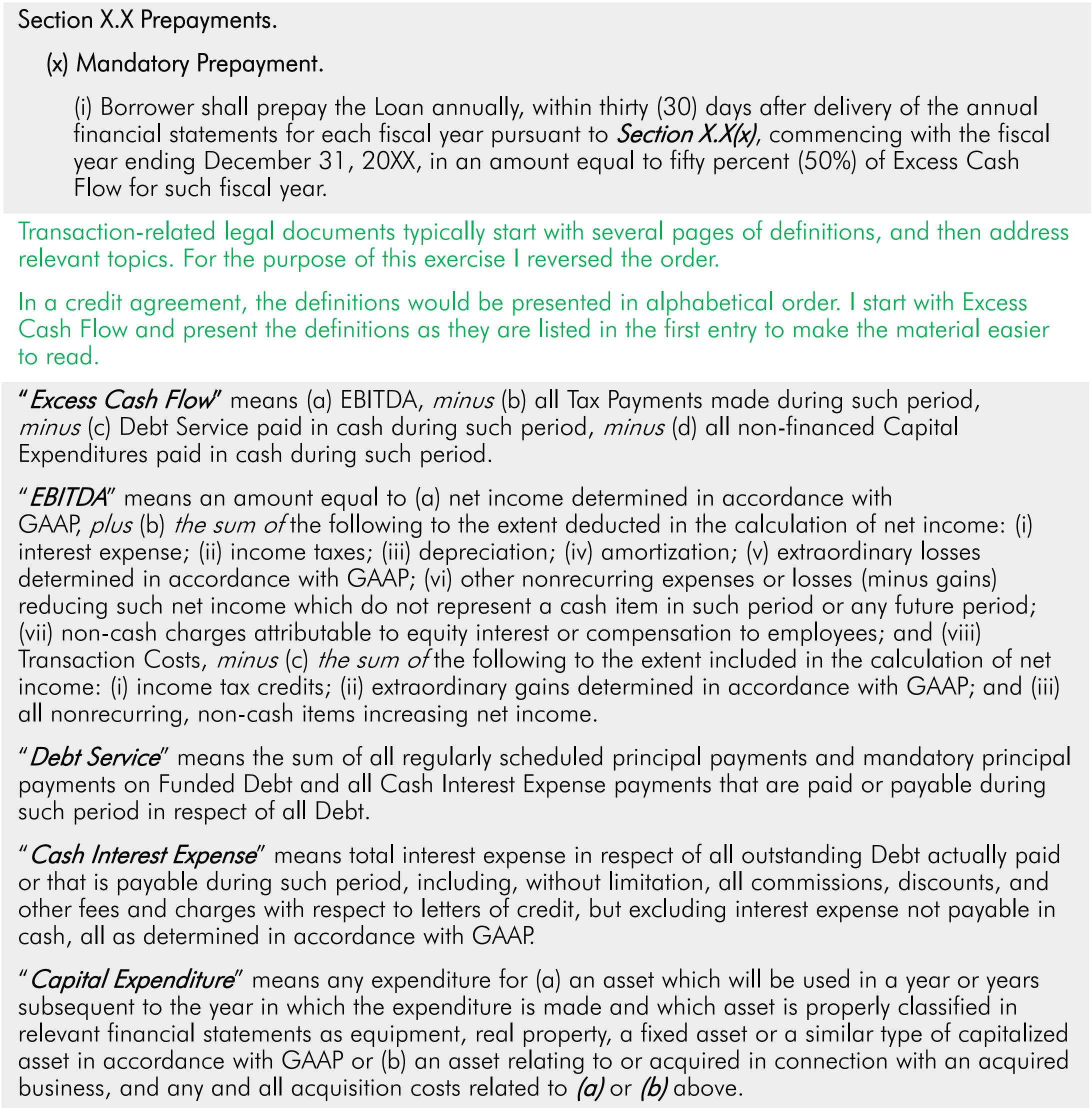

Whereas the first video focused on the mechanics of adding a cash flow sweep, the second video will describe what is taking place in your model. We will also be including notes that explain how this is dealt with at the company level, and some hypothetical language to explain how the cash sweep might appear in a credit agreement (see image that follows).