Private equity due diligence has been traditionally taught with a focus on commercial, financial and legal due diligence. But you will not find a single investor that will downplay the role of management in an operating business, and while information technology (IT) may have been viewed largely as a support function historically, it is increasingly viewed as a driver of growth and value within an organization. For these reasons in this post we will address management due diligence and IT due diligence as well.

Author’s Note: When I first started working in M&A, IT due diligence was frequently grouped under financial due diligence because IT infrastructure supported financial reporting. From the time I transitioned to private equity in 2009, I rarely saw a due diligence process that did not require a separate third party to perform IT due diligence.

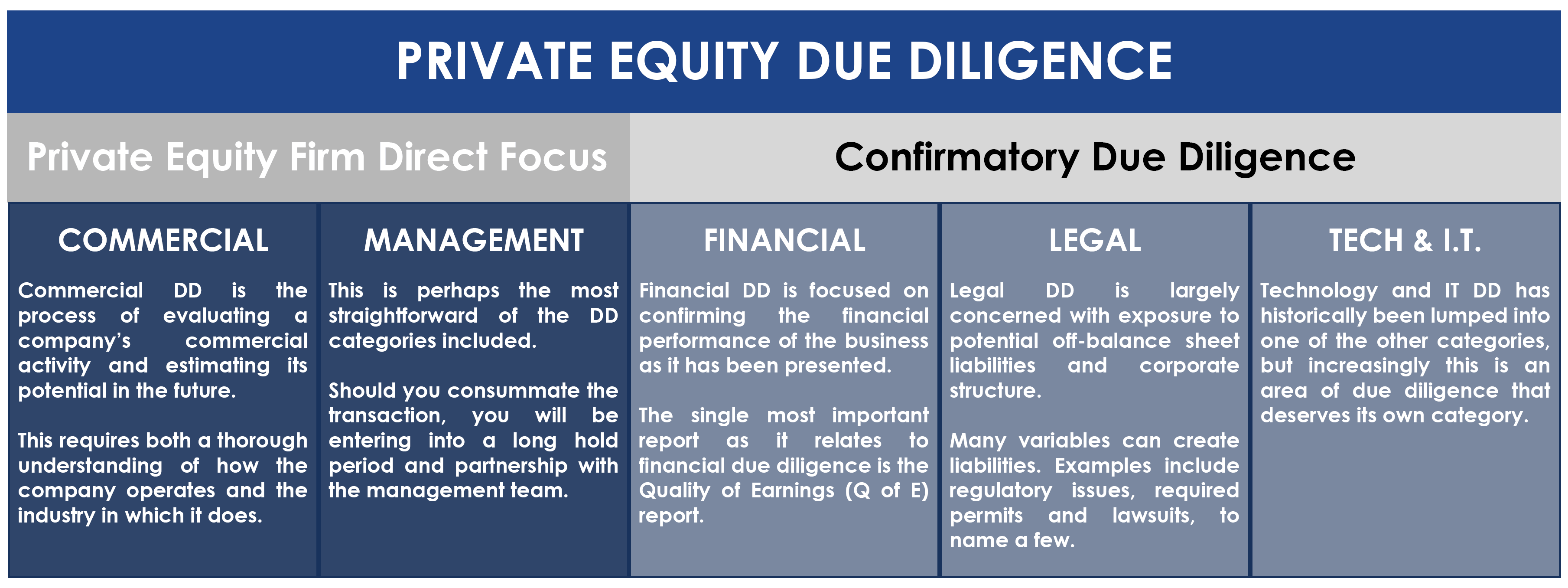

At a more macro level, private equity due diligence should also be divided between confirmatory due diligence and exploratory due diligence. Most exploratory due diligence is focused on commercial and management due diligence, which per the image is where the private equity firm will be most directly involved. At this stage, the investment team is exploring the opportunity as though the information provided is accurate. The objective is to develop the confidence to move forward before engaging third parties to confirm the assumptions supporting the team’s investment thesis.

Confirmatory due diligence is expensive. It involves validating the assumptions supporting the investment thesis, and generally requires engaging third-party specialists. While three of the categories above are exclusively labeled “confirmatory due diligence,” it is possible that all five categories will involve some amount of confirmatory due diligence. With respect to commercial due diligence, and by way of example, a private equity firm can hire a third party to perform industry analysis (see video below) or to perform a customer survey. Some private equity firms, especially those with a strong industry focus may not find this necessary because they have this expertise in house. As it relates to management due diligence, however, in any process it would be irresponsible not to engage a third party to run background checks on the management team.

Due diligence can be highly unpredictable. It is impossible to know everything that will be uncovered in advance, and the time allotted is generally insufficient. Close enough transactions and you are likely to be surprised by findings post close. As such you can only hope to be as thorough as possible in the time available. In the text that follows we will address each of the five topics in summary format. Don’t be intimidated by vocabulary, what follows is simply a description of a highly detailed checklist.

Commercial Due Diligence

Commercial due diligence is the process of evaluating a target company’s commercial activity and estimating its potential in the future. This requires both a thorough understanding of how the company operates and the industry in which it does. The list that follows provides a high-level summary of areas to focus on as part of this process.

- Market Position

- Industry Growth & Landscape

- Customer and Supplier Base

- Financial Performance

- Capital Intensity

Management Due Diligence

In due diligence you should take every opportunity to engage with the management team and get to know them. On this front it is impossible to be sufficiently thorough. In addition to personal interaction and Q&A sessions, the sponsor should also hire a third party to perform background checks.

Pro Tip: I worked with a CEO that in addition to running background checks had a handful of additional data points that he liked to collect for any important hire. A simple but effective data point he developed was to compare the salary the hire claimed to be earning and the salary being offered to the value of the home listed on Zillow for the address on the CV. He would not hire anyone for a role with P&L responsibility if the salary did not comfortably support the value of the home.

Financial Due Diligence

Financial due diligence is focused on confirming the financial performance of the business as it has been presented. This may be confusing because financial performance is included under commercial due diligence as well, but the focus here is on the detail supporting the financial information evaluated in commercial due diligence. By way of example, and in addition to the financial statements listed above, this requires looking at supporting schedules, trial balances, bank statements and audits.

You may have heard that valuation is as much art as it is science. In that context another way to explain the difference is that financial due diligence is the science-heavy component of financial due diligence. Before you can begin to confirm assumptions about how the company operates and develop confidence in projections, you need to know that the data used to create this projection is solid.

Legal Due Diligence

Legal due diligence is largely comprised of “confirmatory” due diligence, which is to say that at this stage the buyer should be highly confident of their decision to move forward absent any new material findings. To confirm assumptions made by the buyer to arrive at valuation, and to confirm that the company is not exposed to large unknown liabilities, the company’s structure and compliance with all laws and regulatory frameworks must be thoroughly evaluated. In the Legal Due Diligence lesson we will explore this process in detail by covering each of the topics that follow:

- General Corporate Information

- Governmental and Regulatory Documents

- Financial Documents

- Litigation Documents

- Business Contracts

- Real Estate and Tangible Assets

- Environmental

- Employee Compensation and Benefit Documents

- Intellectual Property

- Tax Matters

- Insurance

Technology and IT Due Diligence

On the subject of IT due diligence and IT infrastructure more specifically, variations in technology and levels of sophistication between businesses makes it difficult to apply a standardized process (as with much of private equity). That said, for any business dependent on technology the systems supported by IT infrastructure should be evaluated for the following three items: (1) Current Capability, (2) Capacity to Scale, and (3) Risk (Security). To develop an opinion on these three topics, the following items should be thoroughly evaluated:

- Enterprise Applications (e.g. Enterprise Resource Planning (ERP), Supply Chain Management (SCM), Customer Relationship Management (CRM))Network Infrastructure (A diagram should be included.)

- IT Staff and Org Chart

- List all Hardware and Software

- Cyber and Network Security

- Backup and Recovery

- Training (This applies to IT staff, but also to end users. Increasingly firms have in-house cybersecurity training programs.)

While not a comprehensive list, this should provide an idea of some important areas of focus. Increasingly all firms will have a strong technology component to them, and as more software solutions are built for businesses, it will become an ever more important area of due diligence.

This content is a highly summarized version of a more comprehensive lesson available as part of the Private Equity Training curriculum. (Note: related content available as part of the Preliminary Due Diligence and Closing the Transaction courses.)